FAQs

Insurance

What insurance might a business owner, professional or contractor need?

Do business owners and professionals need insurance?

Being a professional carries certain obligations and legal responsibilities. You have a financial responsibility to your client for errors that you make. Although claims are rare, they do happen, and the claims can be very high! Having insurance cover fully protects you and provides you with peace of mind.

I’m new to contracting and want to replace my death in service/employee benefits, what are my options?

This is exactly where we can help! Now you are self-employed, it’s important to ensure you, your business and your loved ones are protected in every eventuality. That could include Income Protection, Critical Illness Cover, Life Insurance, Private Healthcare and Pensions.

What insurance do I need as a business owner, professional or contractor?

The majority of clients legally require you to have some level of Professional Indemnity Insurance, which supports your independent status. Office insurance provides expenses coverage to legally defend or pursue your rights, and Liability Insurance protects damage to both your own and your client’s property or equipment. Also, you should consider protecting your family through insurance; Life Insurance and, specifically, tax-efficient Relevant Life Insurance ensures your loved ones are financially protected in the event of your death. Alongside this is Critical Illness Insurance – protecting yourself and your family if you are ill and no longer able to work and earn.

As a self-employed/limited company business what types of Insurance coverage are compulsory?

It is advisable to consider all elements of insurance to protect you from a variety of risks within your market. If you employ any staff, you are required by law to have Employers’ Liability Insurance.

The only exemptions are limited companies where the owner is the sole employee and unincorporated family businesses where all employees are closely related. Professional Indemnity and Public Liability are often required by your customers under contract.

What insurance policies does an average business owner, professional or contractor take out?

While protection and insurance products are personal, and everyone’s circumstances are different, there are a handful of core products that we see our clients taking out. These include Life Insurance and, specifically, tax-efficient Relevant Life Insurance – which ensures your loved ones are financially protected in the event of your death. Alongside this is Critical Illness Insurance – protecting yourself and your family if you are ill and no longer able to work and earn. Finally, Indemnity Insurance protects your business against any claims made against you.

It’s important to note the value of working with an expert protection adviser firm like Broadbench. We’ll take the time to listen to who you are, and your unique circumstances before designing a protection package that protects exactly what you need it to.

What is Key Person cover?

Key Person Insurance is designed to offer a lump sum or regular monthly income cash injection into a business to mitigate any loss that would occur from either the death or long-term illness of anyone that contributes to the profit of a business.

What is Shareholder Insurance?

Shareholder protection allows business owners to buy shares back from a co-shareholder who is diagnosed with a critical or terminal illness, or dies. This ensures that the deceased owner’s dependants have a willing buyer and cash instead of a share of the business.

What policies can I pay for through my company?

Relevant Life Insurance is a product solely designed for limited company business directors or employees and allows you to expense your Life Insurance through your company, saving you money. Other options of cover, like Critical Illness, Private Healthcare and Income Protection, can be paid for through your company but could be seen as a benefit-in-kind / P11D.

Why should I use an adviser instead of doing it myself online?

A ‘quick quote’ is rarely a good fit for your circumstances. A typical person takes a guesstimate at the amount of cover they need and are led primarily by the monthly premium, rather than ensuring that the policy actually solves the problem they need it to. An adviser is an expert in their field and works hard to understand who you are and your lifestyle so that the policies you take out truly protect you, at a cost that suits your budget.

What’s the point? Insurers don’t pay out

The industry has changed a lot in the last ten years; insurers are now bragging about how many pay-outs they’ve made, rather than avoiding them at all costs. The only thing that hasn’t caught up is their reputation, as many of us still think they’ll argue against any claim made.

I’ve got a medical condition - I won’t be able to get cover

It’s always worth a conversation. In the industry’s move to restore the trust they lost from poor pay-out rates years ago, most have greatly extended the list of illnesses and conditions they cover. This is in line with medical advances too. You could very well get cover for your condition at a reasonable price.

What can I expect to pay?

It’s difficult to say what you can expect to pay for various insurance policies as it is dependent on a number of factors; from your age, health and lifestyle, to your job risk and the amount of cover you want. This is why it’s important to speak to an expert adviser who will ask the relevant questions to help you ascertain what insurance is right for you, and at what price.

My circumstances have changed, should my insurance?

When your circumstances change it’s important to review the policies you have in place. As an example, if you have more children you might want to change the amount of cover you have in place as, if you were to receive a pay-out, this amount might no longer meet your needs. Similarly, if you were downsizing or had paid off a sizable chunk from your mortgage, you might want to reduce the amount of cover you had in place. With any significant life or circumstance changes, make sure you contact your insurance adviser.

What’s the difference between Key Person, Shareholder and Relevant Life Insurance?

Key Person insurance is a policy taken out by a business to compensate that business for the financial losses that would arise from the death (or severe illness) of an important member of the business.

Shareholder Insurance is slightly different in that it allows other shareholders in a business to maintain control following the death (or severe illness) of another shareholder. It helps to avoid instances where a family member of the dead shareholder can take control.

Relevant Life Insurance protects your loved ones, as opposed to your business, in the worst-case scenario. It can cover your mortgage, the cost of raising your children, as well as any other elements of your loved one’s lifestyle that would not be covered should you die. Not only that but it is tax efficient and can be paid for through your company.

Why insurance is so important, both personally and professionally.

Why do we need insurance?

Insurance plans are beneficial to anyone looking to protect their family, assets/ property, and themselves from financial risk/ losses: Insurance plans will help you pay for medical emergencies, hospitalisation, contraction of any illnesses and treatment, and medical care required in the future.

How can insurance companies afford to provide large settlements to the policyholders?

The insurance company collects the premium amount for multiple policyholders and invests the fund securely to accumulate over time and pay out the policyholder when they claim.

How long does it take to arrange cover?

Firstly, we will listen to your specific needs and recommend the right type of insurance to cover your requirements. We will then provide you with the best-suited quotation. If you wish to go ahead with that policy the process takes between 1 to 8 weeks depending on the type of insurance and the complexity of your requirements.

Why should I use you instead of doing it myself online?

If you are looking for a quick quote, you aren’t in the right place! The reason for that is that a ‘quick quote’ is rarely a good fit for what you need. A typical person takes a guesstimate at the amount of cover they need and is led primarily by the monthly premium, rather than ensuring that the policy actually solves the problem they need it to. An advisor is an expert in their field and works hard to understand who you are and your lifestyle so that the policies you take out truly protect you, and at a cost that suits your budget.

What if the policy I take out with you no longer suits me?

Not a problem. We see this as a long-term relationship and will review your circumstances at an appropriate time to assess if anything needs to be adjusted. More importantly, you should be talking to the same person you originally had a conversation with. We certainly aren’t a call centre and are proud of the bespoke and personal nature of our service.

Key Person

What is Key Person Protection?

It’s simply a business insuring itself against the financial loss it may suffer as a result of the death (or critical illness if chosen) of a key person.

Who is a key person?

A key person is an individual whose skill, knowledge, experience or leadership contributes to the continued financial success of the business. A key person may be anyone whose death could lead to a financial loss for the business. This might be a loss of profits if you lost your best salesperson, the cost of having to recruit or train a replacement or important personal or business contracts lost due to the key person not being there to maintain a contract.

How do we prove someone is a key person?

For a business to insure one of its key people it must show that it stands to suffer a financial loss of profits as a result of the death, terminal or critical illness (if chosen) of that employee.

This is usually straightforward, and that individual is then regarded as a key person. The loss of a key person could lead to the business being unable to repay a loan, which could mean the lender calls in the loan early. This may have a serious effect on any existing loans or any future lending.

What types of companies can apply for Key Person Insurance?

Usually, a limited company or a corporation with shareholders whose liability is limited by their shareholdings. Any personal assets are held separately from the finances and assets of the company.

Who pays the premiums for Key Person Insurance?

As the company is the owner of the policy it would usually pay the premiums.

Who receives the pay-out benefits?

In the event of a valid claim, the policy proceeds would be payable to the company.

What is a partnership?

A partnership is a relationship which exists between persons carrying on a business in common with a view to profit. The partnership does not have a separate legal identity and each partner would be liable for any trade debts. It is the partners and not the partnership itself which will own any policy.

Can partners take out Key Person cover on each other?

Yes, a partner could take out their own life policy and place it under trust for the other partners. In the event of a valid claim the policy proceeds would be payable to the trustees who would in turn pay the partners as beneficiaries of the trust. The partnership would usually pay the premiums.

Can partners in Scotland take out Key Person cover on each other?

Yes. In Scotland, a partnership is a separate legal entity and can apply for the policy in its own right. The partnership applies for the policy and completes the policy owner questionnaire. In the event of a valid claim, the policy proceeds would be payable to the partnership. As the partnership is the owner of the policy it would usually pay the premiums.

What happens if the key person leaves or retires?

If a key person were to leave or retire before the end of the Key Person Protection policy term, the business could stop paying the premiums allowing the policy to lapse. Alternatively, the company may choose to continue paying the premiums until the end of the policy term and in the event of a claim, the business would receive a capital sum.

Can Key Person's cover be written in trust?

Yes, the taxation of this can be complicated, for both the company and the life insured. National Insurance, and Capital Gains tax may all need consideration. We strongly recommend that you speak to one of our specialist advisers to guide you through this.

What is the difference between Key Person Insurance and Shareholder Protection?

In many ways these are similar products, they both pay out a lump sum in the event of a claim. The major difference is where the sum assured goes in the event of a claim and the reason each was taken out.

Key Person Insurance is designed to offer a lump sum or regular monthly income cash injection into a business to mitigate any loss that would occur from either the death or long-term illness of anyone that contributes to the profit of a business.

Shareholder Insurance is slightly different in that it allows other shareholders in a business to maintain control following the death (or severe illness) of another shareholder. It helps to avoid instances where a family member of the dead shareholder can take control.

Does your business need Key Person Insurance?

If your business has anyone whose loss, either permanent or temporary would affect the company’s ability to maintain turnover and generate profit then you should explore this protection.

The number of key individuals will vary from one business to another, there is almost always at least one key person in any given business.

Who should be covered by Key Person Insurance?

The obvious choice of key person will normally be some or all of the partners or members in the business. However, it is worthwhile to consider the impact on the business of losing someone who may not have any financial stake in the business but nevertheless plays a fundamental role in its success.

Consider the individuals within your business and ask yourself:

- Would the loss of that person negatively impact or slow down any ongoing projects?

- How easy would it be to replace that person’s expertise?

- Is that individual essential to your business growth?

- Would the loss of that person detriment any customer or supplier relationships?

- Would the business miss their contribution?

- Are there any financial matters, such as bank loans that are dependent upon that key person?

If I don’t take out Key Person Insurance what are the consequences?

The consequences of losing a key person vary on the role of that individual and your business model. There are common factors to consider though, such as without the leadership of you or your key person your employees may decide it’s time for them to move on. Perhaps your customers may choose to go elsewhere and/or your sales revenue could fall. Potentially it could create a lack of confidence from your lender, suppliers, customers, and your other employees. Bank loans and overdrafts could be called in and your suppliers may demand payment upfront.

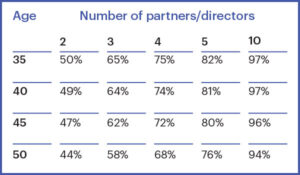

How likely is it that a Key Person will need to Claim?

Likelihood of a Critical Illness – Likelihood of at least one partner or director getting a critical illness before age 65 Source CIBT02 Based on 1971-2003 population data and experience, published in SIAS paper Exploring the critical path, 2006. Males’ standalone, extended cover, including own occupation total and permanent disability.

Likelihood of Death – Likelihood of at least one partner or director dying before age 65 Source www.actuaries.org.uk. Based on mortality data from TMNOO (temporary assured lives, male non-smokers, 1992-2002) at five plus years duration.

How much should I insure my key people for?

There are no hard and fast rules when assessing the financial value of a key person. Each key person must be dealt with on their own merits. A primary method of calculating the key person’s worth is as a multiple of the company profits, the standard multiples are 2 x gross profit or 5 x net profit.

Alternatively, some firms calculate the value as a multiple of that person’s salary. Up to ten times gross salary may be considered for a rapidly expanding business.

Your Broadbench adviser will guide you through this calculation.

What’s the tax position for Key Person Insurance?

Typically, tax relief is not allowed as in nearly all cases the key person being insured is a major shareholder of the business. Just because the policy may not qualify for tax relief does not mean that the company should not take key person insurance. It just means they will not get tax relief on the premiums.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

What do I do if the key person changes their name?

You should notify your insurer’s customer services team or your broker so that the policy details remain up to date. For Broadbench clients, you can update this information on our client portal.

The key person has moved house, how do I update their address details for my Key Person insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Key Person Insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

Life Insurance

What is Life Insurance?

It’s not a nice thing to think about, but if you’re a contractor and you pass away, how would your loved ones survive? This is where Life Insurance can provide the answer. It pays out a large one-off sum to help your family live after you’ve gone.

Do I get any money back if I don't die before the Life Insurance Policy term ends?

No. There’s no cash value at any time. At the end of your Life Insurance policy term, you stop making payments and your cover ends.

Can my mortgage be covered with Life Insurance?

If you have an interest-only mortgage, your outstanding mortgage loan stays the same until you repay it at the end of the mortgage term. Level Life Insurance could cover this type of mortgage.

How does Life Insurance work? What do I need to know?

It provides your loved ones with a large tax-free, one-off payment, or monthly payments if you pass away. It can be used to pay the mortgage off or help your family with living expenses. Monthly payments are tax-deductible if you are a limited company – look at Relevant Life Insurance. You are covered only for the duration (term) of the policy and cover only lasts while you keep up monthly premiums. Monthly payments can be reduced by combining this with a Critical Illness policy.

How do I know what the right policy for me is?

If the unexpected happens, you’d want your family to be taken care of. You’d want the mortgage paid off and enough money for them to live. It’s important to get this right, which is why we work closely with you, making sure the cover fits your needs but is also affordable for you. The policies we recommend are handpicked for business owners, professionals and contractors, and we’ll cut through any jargon, so you know exactly where you stand.

Will my payments on my Life Insurance policy change?

If you choose level or decreasing cover, your monthly payments are guaranteed to stay the same for the duration of your policy.

For decreasing Life Insurance, premiums are set at the start of the policy to consider the decreasing amount of cover you’ll need during the policy term. Premiums for decreasing cover are often cheaper than other types of life insurance.

With level cover, if you choose to help protect your payments from the effects of inflation, so the lump sum won’t be worth less in the future, your monthly payments may rise.

With index-linked cover life insurance, your death benefit increases over the life of the policy. This type of insurance can provide extra protection as the years go by to cover growing expenses, like a new house or bigger family, or protect your death benefit from inflation. The advantage of increasing/ index linked cover term insurance is that you don’t have to predict inflation – the policy will do this for you, but at a cost. Also, your increases are automatic and won’t be hindered if your health changes.

I have a mortgage. Do I need Life Insurance?

If you have a mortgage, you might want to take out Life Insurance. Then, if you die before your policy ends, the lump sum can be used to help pay off the outstanding mortgage balance, so your family could stay in their home. Some lenders will ask you to take out Life Insurance as part of their mortgage offer.

Do I have to take out decreasing Life Insurance to cover a mortgage?

No, you don’t have to take out decreasing Life Insurance to cover a mortgage. The reason for the policy depends on a few factors, such as what you want the lump sum to cover, and how much you want to pay each month. We will advise you on the different levels of cover to suit different needs, so you can choose which one is right for you and your family.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

What do I do if I change my name?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

I've moved house, how do I update my address details for my Life insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Life Insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

Can I cancel my Life Insurance policy at any time?

Yes. You have a 14-day cooling-off period from your policy start date, or from when you get your policy documents (whichever is later), to change your mind. If you want to cancel within this time, we’ll refund any premiums you’ve paid. Remember, there’s no cash value and, if you cancel your policy, you won’t be able to make a claim.

How do I pay for my Life Insurance policy?

You can pay your premiums monthly by Direct Debit.

Is my Life Insurance linked to my mortgage?

We can’t directly link your Life Insurance plan to your mortgage. However, your mortgage lender may register an interest in a portion of the proceeds to cover the remaining cost of the mortgage if you were to die before it’s repaid. But this only acknowledges a third-party interest, and your cover amount still won’t be directly linked to whatever’s left to pay on your mortgage.

Is Terminal Illness Cover included in a Life Insurance policy?

Many Life Insurance policies have the option to include Terminal Illness Cover. Your Broadbench adviser will go through all of the available options with you to ensure the policy meets all of your requirements.

What does my Life Insurance policy cover me for?

You can find out what you’re covered for in the policy documentation. If you’re not sure please contact us.

What’s Life Insurance with decreasing cover?

If you have a Life Insurance plan with decreasing cover, the cover amount decreases over time, broadly in line with the repayment mortgage or long-term loan that you’re repaying. Your premiums stay the same during the term of the policy, unless you make changes to the cover. Decreasing cover usually costs less than level cover.

The policy will pay out if you die, or are diagnosed with a terminal illness and aren’t expected to live longer than 12 months, during the policy term. The policy only pays out once and has no cash value at any time.

What’s Life Insurance with increasing cover?

If you have a Life Insurance policy with increasing cover, the level of cover, and your monthly payments, may increase over time to help protect your cover amount from the effects of inflation.

The policy pays out a lump sum if you die during the policy term, or are diagnosed with a terminal illness and aren’t expected to live longer than 12 months. The policy will only pay out once, so if you make a successful terminal illness claim, a second claim can’t be made. There’s no cash value at any time.

What is Terminal Illness Cover?

Terminal Illness Cover will pay out when you contract an illness/ disease that has no known cure or has progressed to a point where it cannot be cured, and you aren’t expected to live longer than 12 months.

What's the difference between Life Insurance and Over 50s protection?

The main difference is that Life Insurance is a term policy, so it covers you for a specific amount of time, while Over 50s cover is a whole of life policy, so it covers you for the rest of your life.

Typically to take out a Life Insurance policy you need to be aged between 18 and 77 to apply, and your coverage stops at the end of the policy term. You choose a cover amount, and if you want your cover to remain the same, be protected from the effects of inflation, or decrease over time broadly in line with a repayment mortgage or loan. You can take out a single or joint life insurance policy.

If you’re not sure which one might be right for you, speak to a Broadbench financial adviser.

What’s the difference between Relevant Life and Life Insurance?

Life Insurance is cover that you pay for with your own money. However, if you are set up as a limited company, you can pay for your Life Insurance through your business, as a tax-deductible expense, saving you 20%. This is known as Relevant Life Insurance.

How can I set up Life Insurance?

If you’re looking to set up your Life Insurance, our advisers can help you find the right policy for you and your family. Get in touch.

Private Healthcare

What is Private Healthcare?

No one likes being ill but, when you’re a business owner, professional or contractor and your income relies on your ability to work, it’s vital you get back on your feet as soon as possible. A Private Healthcare plan means that you and your family can have access to the best health facilities, without the wait times, so you can protect yourselves from any health issues (and subsequent financial strain) that might come your way.

What does Private Healthcare cover?

Private Healthcare plans are typically designed to cover acute medical conditions. This includes short-term illnesses, treatable diseases and injuries which, through care, you are likely to make a full recovery from. If you have an existing chronic condition, it’s likely that this will be excluded from any cover you take.

Why do I need Private Healthcare?

Unlike other forms of insurance, Private Healthcare tends to be viewed as optional. This is because we are fortunate to live in a country that offers an extensive National Health Service that will cover most treatments for free. However, due to long waiting lists and lack of choice, it could also benefit contractors to have Private Healthcare in place.

As a business owner, professional or contractor, if you can’t work, you can’t earn. With a Private Healthcare policy, you can rest assured that if you do have an illness or injury, you’ll be able to get back on your feet and back to work faster than usual.

Are pre-existing conditions covered?

Private Healthcare is designed to cover conditions that you may develop after taking out the policy. However, depending on the insurer, you may be able to cover pre-existing medical conditions. Keep in mind that this will have an impact on the cost of your premiums.

What are the benefits of Private Healthcare?

Getting help faster – Being seen quickly is one of the many reasons contractors consider Private Healthcare. If you’re unable to earn due to an illness or injury, Private Healthcare will get you back on your feet faster than regular NHS services. You may have access to better care as well as medication and treatments that are not yet available on the NHS.

Privacy and choice – By purchasing Private Healthcare you often have more choice and greater privacy. You may be able to choose a hospital or doctor and even request your own private room – this wouldn’t be available to you if you used the NHS.

What factors affect the premium?

There are many factors that can influence the cost of your premiums. Typically, your age, current health and medical history, but your job may also have an impact if it is seen as a risky profession. If you’re a smoker you may have higher premiums than non-smokers.

What’s important to consider when looking for Private Healthcare?

When looking to get a Private Healthcare policy, it’s important for you to understand what type of cover you require. Do you want comprehensive coverage (which will cover you for everything) or a policy that simply covers you for outpatient visits?

You may also need to consider what could be affecting the price of your premium. Getting the best possible cover won’t be the cheapest but you can’t put a price on your well-being when you’re a contractor. Therefore, it is best to speak to an adviser to find out the level of cover you need to suit you and your circumstances.

How can I set up a Private Healthcare policy?

When it comes to things as important as protecting our health and finances, we believe that you should receive the best impartial advice. To set up a Private Healthcare policy, or if you have more questions and want to speak to an expert, get in touch.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

What do I do if I change my name?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

I've moved house, how do I update my address details for my Private Medical Insurance?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Private Medical Insurance?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

What are the benefits of Private Healthcare?

Getting help faster – Being seen quickly is one of the many reasons contractors, business owners and professionals consider Private Healthcare.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

Critical Illness Cover

What is Critical Illness cover?

Critical Illness cover (also known as Critical Illness Insurance) is a medium to long-term policy which covers you for a serious illness during the policy period so you don’t have to worry about your finances.

How does it work?

If you are diagnosed with a serious illness, a Critical Illness policy will pay out a tax-free, one-off payment (some insurers may offer monthly instalment options also). This can help you pay for your mortgage or rent, and any existing debts you may have or help you to make adjustments to your home, such as a wheelchair ramp if you need it.

Why do business owners, professionals and contractors need Critical Illness?

When you work for yourself, you no longer receive the same benefits as regular employees. These benefits include payment to cover a long period off work due to sickness. The alternative to receiving ‘sick pay’ is to receive state benefits, however, this may not be enough to replace your income.

If you’re eligible, you may be able to receive Employment and Support Allowance (ESA) – which ranges from £70 to just over £100 a week, depending on your circumstances and the seriousness of your illness or disability. Will that be enough to cover your household bills and family’s lifestyle? If not, then you should consider Critical Illness cover.

What illnesses are covered?

Each insurer has its own list of critical illnesses that they cover. Typically, you’ll be insured for heart attacks, cancer (depending on the type and the stage), strokes and permanent disabilities due to an illness or injury. If you have a specific illness that you want to be covered for, get in touch with a Broadbench adviser who will be able to guide you to the right insurer.

What factors impact the policy’s cost?

There are a number of factors that can influence the cost of your monthly premium including:

- Your age

- The level of cover you wish to take out

- Whether you’re a smoker or have previously smoked

- Your current health, weight and family’s medical history

- Your job (some occupations carry higher levels of risk than other professions and therefore may increase the monthly premiums)

What are the benefits of Critical Illness Cover?

Firstly, to keep a roof over your family’s head. With Critical Illness Cover, you can rest assured that you will be able to keep up with mortgage repayments or even pay off the full remaining amount. You’ll receive a tax-free pay-out – If you are diagnosed with a Critical Illness, the money you and your family receive is tax-free. Lastly, it gives you peace of mind – No one knows what the future has in store but with Critical Illness Cover, you will be protected for a number of illnesses. This way you can rest assured that you and your family are financially secure.

You may be able to get small multiple payouts. Most policies will only pay out once, but some insurers will make a small payment if you are diagnosed with a less severe illness. In this case, your policy would continue, and you should be able to make a further claim down the line if you’re diagnosed with a more critical illness.

How is Critical Illness different from Income Protection?

To claim on a Critical Illness policy, you must be diagnosed with a medical condition that meets one of the definitions on the policy. In contrast, to make a claim on an Income Protection policy simply relies upon you being unfit for work, no specific medical condition is needed – therefore the pay-out is to cover you until you’re fit to return to work.

How can I set up a Critical Illness policy?

When it comes to things as important as protecting our health or finances, we believe that you should receive the best advice. To set up a Critical Illness policy, or if you have more questions and want to speak to an expert, get in touch.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

What do I do if I change my name?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

I've moved house, how do I update my address details for my Critical Illness Cover?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Critical Illness Cover?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

Why do contractors need Critical Illness?

When you work for yourself, you no longer receive the same benefits as regular employees. These benefits include payment to cover a long period off work due to sickness. The alternative to receiving ‘sick pay’ is to receive state benefits, however, this may not be enough to replace your income.

If you’re eligible, you may be able to receive Employment and Support Allowance (ESA) – which ranges from £70 to just over £100 a week, depending on your circumstances and the seriousness of your illness or disability. Will that be enough to cover your household bills and family’s lifestyle? If not, then you should consider Critical Illness cover.

Indemnity Insurance

What is Professional Indemnity Insurance?

Indemnity Insurance protects your business against claims made by dissatisfied clients. It will cover your business for the cost of defending any allegations or claims for negligence or breach of duty or care for products or services it has provided. The level of cover you choose can be used to either pay damages awarded against you or cover defence costs (or both) and can in some circumstances be used to ‘fix’ a problem if it will avoid a larger claim being made.

Are all businesses eligible?

These policies are available to UK businesses only.

Who provides the insurance and how can you be so competitive?

Your Broadbench adviser will scour the whole market to find you the best insurance policy to suit your requirements. Broadbench is authorised and registered by the Financial Services Authority.

How can I pay for this insurance?

By direct debit, monthly, quarterly or annually.

What happens when the insurance is due to be renewed?

The policies are continuous, which means they automatically renew. You will be sent a letter with your company details to check. You only need to send this back or contact us if your situation has changed, for example, if your turnover/day rate has increased.

What happens if I have to make a claim under the insurance policy?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

How do I find out the terms and conditions of each type of insurance policy?

We provide a policy summary for each cover when we provide you with your quote which is a plain English overview of the cover listing key benefits, exclusions, claims service information and how to cancel your policy. Some insurance providers will post out your policy documentation and T&Cs, while others make this available online – your Broadbench adviser will tell you how you’ll access your documentation.

How do I cancel or vary the terms of cover?

You should speak to your broker to ensure that either cancelling or amending your cover is the right thing to do.

What is retroactive cover?

This cover provides extra protection for work your business carried out prior to the policy inception date. Unless you specifically request retroactive cover (and provide us with a date to ‘back-date’ your cover to), the policy will only cover work carried out from the inception date of your policy.

The reasons you may want to backdate your cover are; to ensure that you’re covered for work and contracts you have previously entered, or are currently engaged in, and because it could be many months or even years before you are aware of a potential claim arising from work carried out in the past. For example, it might be some time before your client realises they are unhappy with the service you provided.

How can I set up an Indemnity Insurance policy?

When it comes to things as important as protecting our finances and business, we believe that you should receive the best impartial advice. To set up an Indemnity Insurance policy, or if you have more questions and want to speak to an expert, get in touch.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

What do I do if I change my name?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

I've moved house, how do I update my address details for my Indemnity Insurance policy?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Indemnity Insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

Income Protection

What is Income Protection Insurance?

Income Protection is an insurance policy that pays you a regular wage if you’re unable to work due to illness or injury. It will continue to pay you a salary until you’re ready to return to work, retire or if you pass away (dependent on the level of benefit taken).

What does Income Protection cover?

You are covered for most injuries or illnesses, unlike other protection policies. The criteria for a claim within an Income Protection policy is not based on the illness/injury itself but on whether it has stopped you from working.

Will Income Protection protect me if I can’t find a contract?

No. This is a common misconception of Income Protection; it only covers you when you are unable to work due to illness or injury. It does not cover gaps in between employment. If you’re looking for unemployment payment, you will have to apply for JSA.

How much of my pay will be protected?

As a contractor, you can typically ensure between 50% – 80% of your salary and dividends.

What factors impact an Income Protection premium?

Your age, health, line of work and if you have smoked in the last 12 months can have an impact on your monthly premium. Therefore, it’s important to speak to an Income Protection expert to get a rough idea of what cover you can expect and at what cost before applying.

Why is it important for those earning a day rate to have Income Protection?

When you work for yourself, you do not have the financial support of an employer. This means that if you fall ill and are unable to work for a period of time, you do not benefit from sick pay. If this happens, how will you meet your living costs? It’s important to have an Income Protection policy in place so you can meet your living costs (mortgage, bills, food, lifestyle etc) in the unfortunate circumstance of illness or injury.

How long should my deferred period be?

The deferred period is the time between you being unable to work and your payouts beginning. Typically, the longer the deferred period the lower your monthly premiums. To work out the length of your deferred period, you should consider how much you need per month to cover your bills and day-to-day living costs and offset this against your savings. From this, you can work out how long your savings will keep you afloat before you’ll need the financial support a policy delivers.

What happens if I change contracts?

If your new contract pays more or less than the previous contract (or the contract you were on when you started the policy), you can contact your insurer to increase or decrease the amount of coverage you need.

How long can I be covered for?

There are two forms of Income Protection: short-term which typically covers you for 2-5 years and long-term. Long-term will cover you up until an agreed age (usually until retirement). Most contractors take out a long-term policy so that they can be confident they’ll be financially supported in the event of long-term illnesses and injuries.

What do I do if I change my name?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

I've moved house, how do I update my address details for my Income Protection?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Income Protection?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal. Your new Direct Debit will be active within 14 days.

Why do I need Income Protection Insurance?

People in permanent jobs have the benefit of receiving sick pay. Those earning a day don’t have this luxury which is why it’s so important to have Income Protection. It gives you the peace of mind that if you become ill, you’ll be paid a regular wage so you can look after the bills until you’re well enough to return to work.

Can I get Income Protection Insurance if I am self-employed?

Yes, although it’s structured to be paid for personally rather than via a Limited Company.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

How can I set up Income Protection?

If you’re looking to set up your Income Protection, our advisers can help you find the right policy for you and your family. Get in touch and protect your income!

Relevant Life

What is Relevant Life Insurance?

It’s not a nice thing to think about, but if you’re a contractor and you pass away, how would your loved ones survive? This is where Relevant Life Insurance can provide the answer. It pays out a large one-off sum to help your family live after you’ve gone. Plus, a Relevant Life policy offers some very special advantages to limited company business owners and contractors looking for life cover. The headline benefit is tax efficiency.

While the life cover is personal to you, the policy counts as a legitimate business expense, so it is tax deductible. Learn more about how a Relevant Life Policy could be suitable for you by contacting us.

Am I eligible to take out a Relevant Life Insurance policy?

You must have a limited company to benefit from the tax savings that a relevant life insurance policy offers. If you do not have a limited company then standard Life Insurance will offer you the protection you need.

Do I get any money back if I don't die before the Relevant Life Insurance policy term ends?

No. There’s no cash value at any time. Just like standard Life Insurance at the end of your Relevant Life Insurance policy term you stop making payments and your cover ends.

Can my mortgage be covered with Relevant Life Insurance?

If you have an interest-only mortgage, your outstanding mortgage loan stays the same until you repay it at the end of the mortgage term. Level Relevant Life Insurance could cover this type of mortgage.

How does Relevant Life Insurance work? What do I need to know?

Like standard Life Insurance, it provides your loved ones with a large tax-free, one-off payment, or monthly payments if you pass away. It can be used to pay the mortgage off or help your family with living expenses. You are covered only for the duration (term) of the policy and cover only lasts while you keep up monthly premiums. Monthly payments can be reduced by combining this with a Critical Illness policy.

The key difference between Life Insurance and Relevant Life Insurance is that with Relevant Life Insurance the cost of the premiums is moved from your own pocket to your company expenses. This saves you tax and reduces the cost of your monthly premiums.

Additionally, this is not treated as a benefit-in-kind; the premium is not included as a P11D benefit, nor are premiums subject to National Insurance payments for the employer or employee.

There is significant tax relief with a Relevant Life plan and your business can claim Corporation Tax Relief on the premiums. Plus, the payout itself is tax-free.

How do I know what the right policy for me is?

If the unexpected happens, you’d want your family to be taken care of. You’d want the mortgage paid off and enough money for them to live. It’s important to get this right, which is why we work closely with you, making sure the cover fits your needs but is also affordable for you. The policies we recommend are handpicked for contractors, and we’ll cut through any jargon, so you know exactly where you stand.

Will my payments on my Relevant Life Insurance policy change?

If you choose level or decreasing cover, your monthly payments are guaranteed to stay the same for the duration of your policy. For decreasing Relevant Life Insurance, premiums are set at the start of the policy to consider the decreasing amount of cover you’ll need during the policy term. Premiums for decreasing cover are often cheaper than other types of life insurance.

With level cover, if you choose to help protect your payments from the effects of inflation, so the lump sum won’t be worth less in the future, your monthly payments may rise. The maximum annual increase would be 15% to your premiums and 10% to your cover.

Who do I notify in the event that a policyholder passes away?

You should notify the claims department of your insurer, you will find this contact info on the policy documents or their website.

What do I do if I change my name?

You should notify your insurer’s customer services team or your broker so that your details remain up to date. For Broadbench clients, you can update this information on our client portal.

I've moved house, how do I update my address details for my Relevant Life insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

What should I do if my bank details change for my Relevant Life Insurance policy?

You should notify your insurer’s customer services team or your broker so that your policy doesn’t lapse. For Broadbench clients, you can update this information on our client portal.

Can I cancel my Relevant Life Insurance policy at any time?

Yes. You have a 14-day cooling-off period from your policy start date, or from when you get your policy documents (whichever is later), to change your mind. If you want to cancel within this time, we’ll refund any premiums you’ve paid. Remember, there’s no cash value and, if you cancel your policy, you won’t be able to make a claim.

How do I pay for my Relevant Life Insurance policy?

You can pay your premiums monthly by Direct Debit.

Is Terminal Illness Cover included in a Relevant Life Insurance policy?

Many Life Insurance policies have the option to include Terminal Illness Cover. Your Broadbench adviser will go through all of the available options with you to ensure the policy meets all of your requirements.

What is Terminal Illness Cover?

Terminal Illness Cover will pay out when you contract an illness/ disease that has no known cure or has progressed to a point where it cannot be cured, and you aren’t expected to live longer than 12 months.

What does my Relevant Life Insurance policy cover me for?

You can find out what you’re covered for in the policy documentation. If you’re not sure please contact us.

What’s Relevant Life Insurance with decreasing cover?

If you have a Relevant Life Insurance Plan with decreasing cover, the cover amount decreases over time, broadly in line with the repayment mortgage or long-term loan that you’re repaying. Your premiums stay the same during the term of the policy, unless you make changes to the cover. Decreasing cover usually costs less than level cover.

The policy will pay out if you die, or are diagnosed with a terminal illness and aren’t expected to live longer than 12 months, during the policy term. The policy only pays out once and has no cash value at any time.

What’s Relevant Life Insurance with increasing cover?

If you have a Relevant Life Insurance policy with increasing cover, the level of cover, and your monthly payments, may increase over time to help protect your cover amount from the effects of inflation.

The policy pays out a lump sum if you die during the policy term, or are diagnosed with a terminal illness and aren’t expected to live longer than 12 months. The policy will only pay out once, so if you make a successful terminal illness claim, a second claim can’t be made. There’s no cash value at any time.

What's the difference between Relevant Life Insurance and Over 50s protection?

The main difference is that Relevant Life Insurance is a tax-efficient term policy, so it covers you for a specific amount of time, while over-50 life insurance is a whole of life policy, so it covers you for the rest of your life.

Typically to take out a Relevant Life Insurance policy you need to be aged between 18 and 77 to apply, and your coverage stops at the end of the policy term. You choose a cover amount, and if you want your cover to remain the same, be protected from the effects of inflation, or decrease over time broadly in line with a repayment mortgage or loan. You can take out a single or joint life insurance policy.

If you’re not sure which one might be right for you, speak to a Broadbench financial adviser.

What’s the difference between Relevant Life and Life Insurance?

Life Insurance is cover that you pay for with your own money. However, if you are set up as a limited company, you can pay for your Life Insurance through your business, as a tax-deductible expense, saving you 20%. This is known as Relevant Life Insurance.

How can I set up a Relevant Life Insurance policy?

If you’re looking to set up your Life Insurance, our advisers can help you find the right policy for you and your family. Get in touch.

Mortgages

Buy to Let

What is a Buy To Let mortgage?

A Buy to Let mortgage is where you buy another property specifically as an investment with the intention of letting it out.

How much deposit do I need for a Buy to Let mortgage?

Normally a minimum of 25% deposit.

Is there any tax to pay when I sell my property?

Not for your main residence, but if you have investment properties that were bought on a Buy to Let basis, these will be subject to Capital Gains Tax. Other taxes may also be levied, we recommend you speak with an accountant to establish your tax position.

Can I get a mortgage if I earn a day rate, rather than PAYE?

Yes. Of course, there are factors that impact a contractor’s eligibility, but just by being self-employed, you should not expect to be turned down by a lender as long as they understand contractors and contracting. However, factors that would prevent anyone from securing a mortgage, such as a poor credit history or a bad payment record will apply just as much. to contractors as to employees.

Can I get a mortgage if I have only just started contracting?

Yes! As long as we can see you’ve got a history in the same line of work and in the same industry in which you are now contracting, there are lenders who accept new contractors.

What is the Mortgage process?

A typical journey will look like this:

- Welcome Call

This is an introductory meeting. You’ll meet your Broadbench adviser: they’ll explain our services, our regulatory status and establish a basic understanding of your requirements. - Fact-find

Your adviser will send you a fact-find document for you to complete. Once received, your adviser will schedule a Discovery Call. - Discovery and Recommendation Call

We’ll confirm the details supplied in the fact-find, and discuss your mortgage options: fixed/tracker, term, fees, and your budget. Your adviser will also advise you about life insurance products to protect the mortgage and your family’s lifestyle.Your adviser completes your mortgage recommendation and the KFI (Key Features Illustration) and then will advise you on the AIP process. You’ll both agree what are the next steps: house hunting or booking your mortgage. - AIP (Agreement In Principle)

Your adviser will send you an invoice of £100 to create the AIP. Once payment is received the AIP can be booked. - Documentation

Then adviser will send you a checklist of all the documentation you need to supply to us. You’ll then be invoiced for the remaining £400. - Mortgage Offer

Once all documents are received, we’ll certify that your mortgage is ready to be booked. Your adviser then books your mortgage. Once the mortgage offer is received, we’ll liaise with the lender on your behalf. - Mortgage Review

You let us know your exchange and completion dates. - Mortgage Completion

We’ll let you know as soon as your mortgage completes and then schedule regular reviews during the mortgage term to ensure that the product remains the most suitable for you.

Why should I use a specialist broker?

By all means, go to a high street lender to satisfy your curiosity, but in most cases, the lender will have issues with how income reaches the contractor. High street lenders understand dividends, but business owners, professionals and contractors who are tax efficient and only draw down a minimum salary and dividends to meet their needs won’t look good. Specialist brokers like us go to the same lenders you see in the high street but at the head office underwriter level. This means they are speaking to people with a bigger lending mandate and a knowledge of this sector contractors, and they use the contract to define a contractor’s income.

Remortgages

What happens when my fixed-rate mortgage deal comes to an end?

If you’re currently on a fixed rate mortgage, it means for a period of time (typically between 2-5 years) the interest you pay and the monthly repayment will be fixed. Once your fixed mortgage deal comes to an end, you will be placed on the ‘Standard Variable Rate’ (SVR). Each lender sets their own SVR and it tends not to be as competitive as fixed-rate mortgages.

I was permanent when I took out my mortgage but now I am earning a day rate. Will I be accepted for a remortgage as a contractor?

You will still be able to get a mortgage however, your existing lender might not be able to understand your income now you’re contracting. It’s important to speak to a specialist contractor mortgage adviser who works with the whole of market and will find a lender that can understand your income and make sure you’re getting the best mortgage product available.

How much could I save by remortgaging?

It’s important to speak to a specialist mortgage adviser who works with the whole of market.

What documents do I need to remortgage?

If you’re switching to a new lender, the documents you need to provide will be similar to when you applied for the first mortgage. This will include details of your current and previous contract (if applicable), 3 months’ bank statements and if you have less than 3 months remaining on your contract, they will require a contract extension.

Are there any charges for remortgaging?

There are some fees to be aware of when remortgaging, for example, some lenders have upfront product fees that can be added to the loan, usually about £1000. Lenders do offer a free legal and valuation service to help you switch. If you’re not sure whether you’d want to pay a product fee, a mortgage specialist can help you look through the options.

Can I borrow more by remortgaging?

A great benefit of remortgaging is that it gives you an opportunity to borrow more money. This can be used to make home improvements such as building an extension or refurbishing the kitchen or bathroom. Make sure you speak to an expert mortgage adviser to help assess how much you can borrow based on your day rate.

Where can I find the best rate?

This is where we can help. Scouring the market for the best mortgage product can be a long and difficult process and, unless you have the right expertise, you may not end up with the best deal for you. Our specialist mortgage advisers do all the leg work, working with contractor-friendly lenders, so you don’t have to. Speak to your Broadbench adviser and see how much you could save on your remortgage.

Home Mover

Why should I use a specialist Contractor broker?

By all means, go to a high street lender to satisfy your curiosity, but in most cases, the lender will have issues with how income reaches the contractor. High street lenders understand dividends, but business owners, professionals and contractors who are tax efficient and only draw down a minimum salary and dividends to meet their needs won’t look good. Specialist brokers like us go to the same lenders you see in the high street but at the head office underwriter level. This means they are speaking to people with a bigger lending mandate and a knowledge of this sector contractors, and they use the contract to define a contractor’s income.

Do I qualify to be assessed for a mortgage on contract value?

Lenders who specialise in mortgages for those earning a day rate typically assess the amount that can be borrowed on the annualised contract value. Each client is evaluated on the basis of their personal circumstances, generally, they can borrow a multiple of their annualised contract value.

However, they need to be in a contract at the time of the application and must be able to demonstrate continuity. A contractor applying with their first contract can get a mortgage as long as they have had continuity of employment before approaching the broker.

How long does the mortgage application process take?

This is where a contractor specialist financial adviser differs from most brokers. There is a two-stage process. The first stage is the pre-approval, and the second stage is the full application.

In stage one, the lender requests documents from the business owner, professional or contractor such as current and previously signed contracts, three months’ personal and business bank statements, ID and proof of address. The lender will also complete a hard credit search at the point of application. After reviewing all documents and credit score, the lender will approve or decline the application.

Stage two is the full application stage. If the application has been approved the valuation will then be instructed, and if the valuation is satisfactory, the mortgage will go to offer. In some examples, the mortgage loan amount may be reduced following an underwriting review or the mortgage can be declined. Your broker would then agree with you on how you wish to proceed.

I have a poor credit history – can you get me a mortgage?

Brokers do have options for contractors who have a poor credit history and need specialist contractor underwriting for their mortgage. They will need to present a relatively positive picture of the client’s current circumstances and as long as the credit issues are historic and there has not been an issue within the last two years, but can usually find an option.

There are lenders who don’t do credit scoring but just complete credit checks. Financial advisers like Broadbench, with unrestricted access to the market and who are not restricted to just a handful of lenders, should be able to find a solution. However, the contractor will pay a premium with an elevated interest rate as a result of their poor credit history.

If a contractor has any plans to buy a property or refinance it is important that they talk to a specialist contractor financial adviser as early as possible, even if their plans are 12 months away.

That way the broker can find out early if there are any challenges and we can overcome them in plenty of time for the contractor to secure their mortgage when they need it.

What evidence do you need of my contracting income?

It depends on the lender; however, most will ask for your current contract, your previous contract (if applicable), a contract extension (if you have less than 3 months remaining on your contract) and 3 months of business bank statements.

How do the lenders calculate my income?

The lenders take your day rate or hourly rate and times this by how many days/hours a week you work and times that by 46 or 48 weeks a year (lender dependent). This is then deemed your annual salary.

First Time Buyer

Why is the area so important?

From crime to community, amenities to areas of green space. Good questions to ask include: where is the nearest supermarket or is the corner shop within walking distance or will you have to drive? Where’s the closest bus stop or train station? How are the local schools rated by Ofsted?

How much can I borrow?

The main things that dictate how much a person or couple can borrow is income and current credit commitments. All lenders have different ways to calculate what someone can borrow.

How much deposit do I need?

You will need a minimum of a 5% deposit. The more deposit you put in, the better the interest rates will be. For example, if you put in a 15% deposit this will get you a better interest rate than a 10% deposit.

What is the difference between a repayment mortgage and an interest-only mortgage?

A repayment mortgage is guaranteed to pay off your mortgage by the end of the term as long as all payments have been made.

An interest-only mortgage is where your monthly payments are only covering the cost of the interest and your loan amount will remain the same. At the end of the term, you would either need to sell the property to repay the mortgage or find another source to repay the loan.

What insurance do I need for a mortgage?

As a minimum, the building itself needs to be insured. We would usually recommend that you also insure the contents within your home too. Other insurances we recommend are Life Insurance to repay the mortgage debt if someone passes away and Income Protection insurance which provides you with an income should you be unable to work due to sickness or accident.

Can I move my mortgage to another lender if they are offering a better interest rate?

Yes. You can “remortgage” to another lender to take advantage of their better interest rates. As part of our service, we will contact you as you approach the final few months of your existing mortgage deal to provide you with details of the options available to you.

Can I get a mortgage if I earn a day rate, rather than PAYE?

Yes. Of course, there are factors that impact a contractor’s eligibility, but just by being self-employed, you should not expect to be turned down by a lender as long as they understand contractors and contracting. However, factors that would prevent anyone from securing a mortgage, such as a poor credit history or a bad payment record will apply just as much. to contractors as to employees.

Looking to remortgage

What is remortgaging?

Remortgaging is the process of switching your existing mortgage product to a new mortgage product, either with your existing lender or a new lender.

What happens when my fixed-rate mortgage deal comes to an end?

If you’re currently on a fixed rate mortgage, it means for a period of time (typically between 2-5 years) the interest you pay and the monthly repayment will be fixed. Once your fixed mortgage deal comes to an end, you will be placed on the ‘Standard Variable Rate’ (SVR). Each lender sets their own SVR and it tends not to be as competitive as fixed-rate mortgages.

I was permanent when I took out my mortgage but now I am contracting. Will I be accepted for a remortgage as a business owner, professional or contractor?

Those earning a day rate will still be able to get a mortgage however, your existing lender might not be able to understand your income now you’re contracting. It’s important to speak to a specialist mortgage adviser who works with the whole of market and will find a lender that can understand your income and make sure you’re getting the best mortgage product available.

How much could I save by remortgaging?

It’s important to speak to a specialist mortgage adviser who works with the whole of market.

What documents do I need to remortgage?

If you’re switching to a new lender, the documents you need to provide will be similar to when you applied for the first mortgage. This will include details of your current and previous contract (if applicable), 3 months’ bank statements and if you have less than 3 months remaining on your contract, they will require a contract extension.

Are there any charges for remortgaging?

There are some fees to be aware of when remortgaging, for example, some lenders have upfront product fees that can be added to the loan, usually about £1000. Lenders do offer a free legal and valuation service to help you switch. If you’re not sure whether you’d want to pay a product fee, a mortgage specialist can help you look through the options.

Can I borrow more by remortgaging?

A great benefit of remortgaging is that it gives you an opportunity to borrow more money. This can be used to make home improvements such as building an extension or refurbishing the kitchen or bathroom. Make sure you speak to an expert mortgage adviser to help assess how much you can borrow based on your day rate.

Where can I find the best rate?

This is where we can help. Scouring the market for the best mortgage product can be a long and difficult process and, unless you have the right expertise, you may not end up with the best deal for you. Our specialist contractor mortgage advisers do all the leg work, working with day rate friendly lenders, so you don’t have to. Speak to your Broadbench adviser and see how much you could save on your remortgage.

Important mortgage questions

Can I get a mortgage if I earn a day rate, rather than PAYE?

Yes. Of course, there are factors that impact a contractor’s eligibility, but just by being self-employed, you should not expect to be turned down by a lender as long as they understand contractors and contracting. However, factors that would prevent anyone from securing a mortgage, such as a poor credit history or a bad payment record will apply just as much to contractors as to employees.

Can I get a mortgage if I have only just started contracting?

Yes! As long as we can see you’ve got a history in the same line of work and in the same industry in which you are now contracting, there are lenders who accept new contractors.

What is the Mortgage process?

A typical journey will look like this:

- Welcome Call

This is an introductory meeting. You’ll meet your Broadbench adviser: they’ll explain our services, our regulatory status and establish a basic understanding of your requirements. - Fact-find

Your adviser will send you a fact-find document for you to complete. Once received, your adviser will schedule a Discovery Call. - Discovery and Recommendation Call

We’ll confirm the details supplied in the fact-find, and discuss your mortgage options: fixed/tracker, term, fees, and your budget. Your adviser will also advise you about life insurance products to protect the mortgage and your family’s lifestyle.Your adviser completes your mortgage recommendation and the KFI (Key Features Illustration) and then will advise you on the AIP process. You’ll both agree what are the next steps: house hunting or booking your mortgage. - AIP (Agreement In Principle)

Your adviser will send you an invoice of £100 to create the AIP. Once payment is received the AIP can be booked. - Documentation

Then adviser will send you a checklist of all the documentation you need to supply to us. You’ll then be invoiced for the remaining £400. - Mortgage Offer

Once all documents are received, we’ll certify that your mortgage is ready to be booked. Your adviser then books your mortgage. Once the mortgage offer is received, we’ll liaise with the lender on your behalf. - Mortgage Review

You let us know your exchange and completion dates. - Mortgage Completion

We’ll let you know as soon as your mortgage completes and then schedule regular reviews during the mortgage term to ensure that the product remains the most suitable for you.

Will high street lenders consider those earning a day rate? Will I be with a specialist lender at a higher rate of interest?

There are high-street lenders that accept those outside of PAYE, the problem is that a lot of brokers don’t necessarily know how to package contractor applications correctly! That’s where a specialist adviser comes into play.

Why should I use a specialist broker?

By all means, go to a high street lender to satisfy your curiosity, but in most cases, the lender will have issues with how income reaches the contractor. High street lenders understand dividends, but business owners, professional and contractors who are tax efficient and only draw down a minimum salary and dividends to meet their needs won’t look good. Specialist brokers like us go to the same lenders you see in the high street but at the head office underwriter level. This means they are speaking to people with a bigger lending mandate and a knowledge of this sector, and they use the contract to define a contractor’s income.

Do I need three years of company accounts before I apply?

Whereas that might have been the case several decades ago, this is certainly no longer true.

What evidence do you need of my contracting income?

It depends on the lender; however, most will ask for your current contract, your previous contract (if applicable), a contract extension (if you have less than 3 months remaining on your contract) and 3 months of business bank statements.

How do the lenders calculate my income?

The lenders take your day rate or hourly rate and times this by how many days/hours a week you work and times that by 46 or 48 weeks a year (lender dependent). This is then deemed your annual salary.

Will I qualify for a competitive interest rate deal?

Not only can business owners, professionals and contractors qualify for the same sort of rates as employees. When viewed as a whole, this lending market shows typically much lower rates of mortgage default than the wider market.

This makes those earning a day rate less risky than other lending groups. Not every lender has realised the benefits of lending to contractors, but there is no dual pricing for employees versus contractors.

Will I need a higher deposit because I’m a contractor and perhaps be seen as a higher risk?

Lenders are understanding that more and more people are opting for contracting rather than permanent positions and, therefore, don’t penalise you for this. Some lenders will consider up to a 95% loan with as little as a 5% deposit.

I retain a lot of money in my business and withdraw only what I need, will this affect my ability to get a mortgage?

As long as we can evidence the money coming in via your business bank statements and your day rate is evidenced on your contract, this will be acceptable to the lenders. They understand that you are drawing money tax efficiently and that you have the flexibility of drawing more out if you needed to.

What does ‘self-certification’ mean?

‘Self-certification’ was what the self-employed, small business owners and contractors used to do to prove their incomes. The practice of self-certification was banned in 2008 by the regulator at the time, the Financial Services Authority.

How is my application going to be looked at?

This is an important question for contractors because many don’t quite know how to describe their employment status. It is actually quite straightforward for those earning a day rate who are receiving the right advice, as most lenders now recognise a ‘third way’ for business owners, professionals and contractors.

Even though umbrella company contractors are employed by their umbrella company service provider and limited company contractors are similarly employed by their limited company and contractors are typically not self-employed sole traders, more and more lenders are recognising professional contractors as a valid third way, and a much safer lending risk.

Do I qualify to be assessed for a mortgage on contract value?

Lenders who specialise in mortgages for those earning a day rate typically assess the amount that can be borrowed on the annualised contract value. Each client is evaluated on the basis of their personal circumstances, generally, they can borrow a multiple of their annualised contract value.

However, they need to be in a contract at the time of the application and must be able to demonstrate continuity. A contractor applying with their first contract can get a mortgage as long as they have had continuity of employment before approaching the broker.

How long does the mortgage application process take?

This is where a specialist financial adviser differs from most brokers. There is a two-stage process. The first stage is the pre-approval, and the second stage is the full application.